I wear two hats: a fintech entrepreneur and an angel investor. Also, I’ve spent the last 15 years investing and trading in various types of securities in public markets and worked in £bn+ public to private transactions.

Over the past 18 months we at CityFALCON have raised £400K in two rounds. During that process I’ve met with at least 50+ investors, from angel investors, VCs, and family offices. Our company has won several awards and gotten some positive press, so there’s been a lot of interest in us. But even with all that, fundraising has been a real b*tch.

There’s a lot said about the conservative nature of investors in the UK and Europe compared to our friends in Silicon Valley or New York – and it’s not all unfounded. But I’ve been on both sides of the fence, so I know it’s not all the fault of timid investors. We entrepreneurs are doing several things wrong.

- There is ‘no risk of losing out’ in the UK and Europe

When does an investor actually sign the cheque to invest in a company, be it public or private? Most times it’s when they have a fear of losing out on an opportunity. For example, Oil is below $30 and everyone knows there is value there, because of the cost of production and the long term demand-supply dynamics. But how many of the investors and traders are buying Oil? Everyone wants to be part of the bounce back, but are waiting till the time they see some positive momentum.

- There have been very few exits compared to the number of start-ups raising funds

In the UK, you don’t hear stories about people investing £10K in a start-up and then exiting for £100,000 – seemingly a regular occurrence in the Valley. It’s tempting to blame entrepreneurs for this, but that’s not the whole story. The key reason for this is we don’t have the start-up ecosystem of mentors, investors and employees who have built or worked in start-ups. In the UK we lack the experience and support of people who have gone through the different phases of growth and had their own successes and failures. We do have some ‘smart’ investors here, and we’re lucky for it, but most of the money in the UK is ‘dumb’ money.

As it stands, a rational investor would stay away from start-ups. Most of the time, investing in startups is mostly for the tax benefits (SEIS, EIS, etc.).

- Forget exits, some entrepreneurs do not even update their investors on a regular basis

One of the most frustrating things angel investors face in the UK is not getting updates from a company they have invested in. Imagine the unease these investors would feel about putting money into more start-ups. And ask yourself how likely someone is to give follow up investment after receiving no updates. At CityFALCON, I get the team to provide me with all metrics so that we send an update within 5 days of close of each month. It’s vitally important, and not that difficult!

- It’s become an investors’ market at an early stage

There’s a popular misconception built by the media that the UK has an abundance of money, just waiting for hungry entrepreneurs to come and grab it all. This has led to entrepreneurs from all over Europe and Asia looking to raise capital in the UK. While there is money in the UK, a lot of it isn’t for you. The traditionally risk averse investors in the UK, coupled with the flood of some of the best entrepreneurs from all over the world has given investors more choice, and made it more difficult for many start-ups to get off the ground.

- Hustling is fine but spamming investors to raise funds is not cool

Every two or three days, I get an email that says something like, “We are closing our EIS round, expected ROI of x%….”. Most of the angel investment works on references, and I’m not sure how many entrepreneurs get funding using this approach. It’s like bombarding your CV to 200 companies when you’re looking for a job.

There is a lot we entrepreneurs can learn about building relationships from business development executives. The successful ones don’t start selling from my their first sentence, they first work on building a rapport, a connection with the potential customer.

It’s not abundance but scarcity of assets that drives up its value. Let the investors chase opportunities instead of us chasing them.

- Be ready to walk away

Some potential investors will take up too much of your time. They will request tons of documents and information without any real intention of investing in the company. I’ve been guilty of this too. Most of the investment we raised came with less than three meetings with the potential investor. We need to go back to the basics of negotiating.

Late-stage and “successful” entrepreneurs are giving too much away

- Several in-demand start-ups are undervalued

Take a company like Crowdcube. Their fundraise was subscribed in 15 minutes. In pure finance terms, they left too much on the table. They could have raised money at a much higher valuation. This has been the case with Seedrs, and other popular brands that have raised funds and have been oversubscribed. I’m hoping that crowdfunding sites in the future will start thinking about the basic principles of demand and supply, and have a book-building process on the site.

- Late-stage investors want upside of common equity with downside protection of debt – real expensive capital

One of the biggest shocks for me after entering the entrepreneurial world was the term sheets that entrepreneurs are forced to sign. In the public markets when you’re buying a share in a company, you get equity in the company at the same terms as other investors. But in the start-up world, late stage investors who face less risk than early-stage investors, employees, and entrepreneurs, demand preferential liquidations, warrants, etc. The sad part of it all is that this has become accepted and most people think that it’s fair! Unfortunately, most of us will have to sign these term sheets, because they have become the standard, but do remember that you are giving too much away.

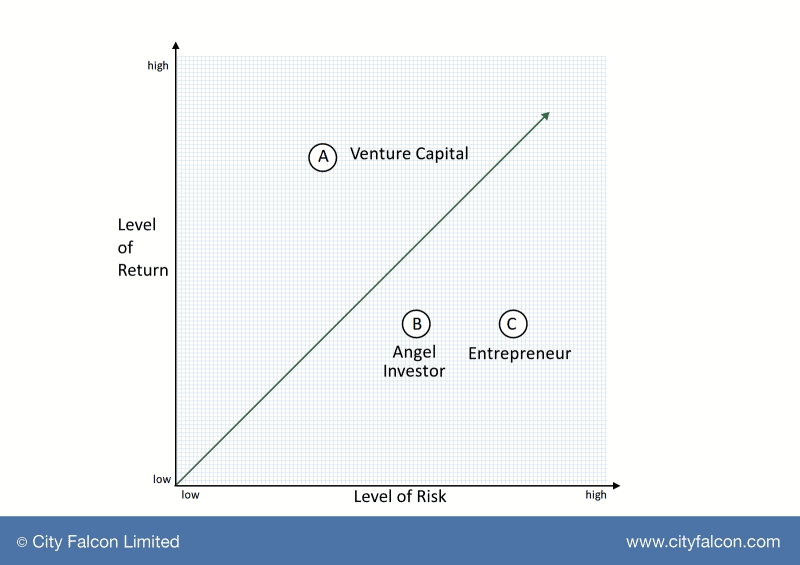

The graph below shows the risk-return profile of debt and equity in public markets.

Since most late-stage investors are getting a great deal during investments, this is what their position looks like on the same graph

With venture capital getting preferential rewards, the risk reward mix for entrepreneurs, employees and early angel investors becomes unfavourable, though some of the angel investors’ risks are reduced due to tax schemes such as SEIS and EIS.

Why would late stage investors want to move early when they can get a favourable risk reward ratio from start-ups that have already been successful enough to reach the Series A stage and beyond?

My appeal to all entrepreneurs

Investors sit in a room, judge start-ups and work together to collectively decide whether to invest in pitching companies. It’s time for entrepreneurs to come together and improve the fundraising environment for ourselves and other companies that will raise funds after us.

We need the support of late stage entrepreneurs who are successful to offer the same risk-reward profile to VCs and late stage investors as they do to the early stage investors and their employees. This may result in some of these late stage investors moving to early stage to generate potential higher returns. And of course, you’ll show that you care about those who supported you in the first place: your early stage investors and your employees.

Leave a Reply